Use Case: Carbon Impact

Deliver mail digitally - cut your carbon footprint

Is paper mail holding back your sustainability goals? Make the switch to secure email and take a meaningful step toward Net Zero.

%20(1).webp?width=938&height=563&name=Financial%20services%20leader%20on%20the%20phone%20talking%20about%20secure%20email%20sustainability%20(1)%20(1).webp)

The Road to Net Zero

Reaching Net Zero by 2050 means rethinking how we send information. We worked with Project Rome’s Professor Simon Pringle to compare the carbon impact of paper mail and secure email.

View our findings

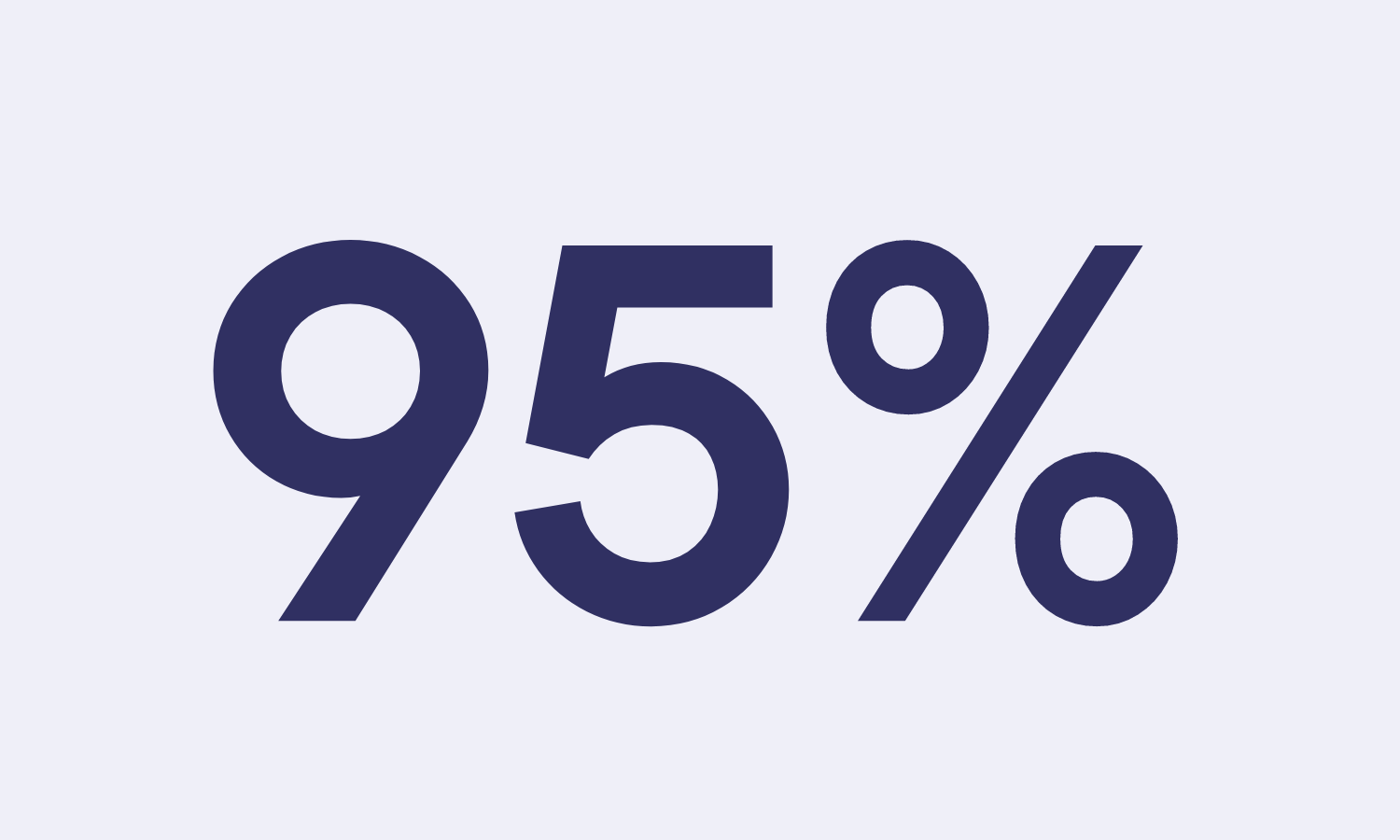

95% lower costs

Our consultancy process revealed that businesses with high mail volumes can save up to 95% on print, pack, and post by switching to secure email.

80% carbon reduction

Secure email reduces carbon output by over 80% when accounting for the full lifecycle of paper production and delivery.

270 tonnes of CO₂ saved

Aegon has saved an estimated 270 tonnes of CO₂ since switching to Mailock in 2019.

Time to change?

Switching even part of your sensitive document output to secure email is a step forward - not just for the planet, but for your organisation’s security and compliance posture as durable-medium rules increasingly favour digital delivery.

Carbon footprint

Every tonne of post generates around 3 tonnes of CO₂e & uses around 1,000 tonnes of water.

Rising costs

Paper prices rose by 60% in 2022. Royal Mail delivery costs increased between 10 and 18%.

Service interruptions

Postal strikes and cyber attacks have led to delays, lost documents, and customer dissatisfaction.

Legacy inefficiency

In a digital-first world, postal delivery introduces unnecessary delays to time-critical communications.

Security risk

Confidential post can be opened by anyone who handles it, putting customer data at risk.

Compliance issues

Once a letter is sent, there’s no way to control access in the event of a breach. Regulators such as the FCA increasingly recommend a 'digital by default' approach.

Switch from recorded post to secure email

Mailock enables organisations to send confidential communications securely to customers’ inboxes - cutting carbon, reducing risk, and boosting efficiency.

High response rates

Deliver direct to the email inbox and increase open and response rates.

Easy deployment

Integrate with your mail flow or ask your document production provider about integrating Mailock.

Managed service

Use our managed cloud platform or host the solution on-premise with Enterprise support.

Kim

Mailock recipient

Clarissa

Mailock Recipient

James

Mailock Recipient

Chris

Mailock recipient

Heather

Mailock recipient

Charlie

Mailock recipient

Pro

For regulated teams and professionals

Protect sensitive emails with advanced tools for encryption, authentication, and message control in Outlook or web.

.png?width=900&height=525&name=Customer%20service%20agent%20smiling%20in%20office%20with%20colleagues%20(1).png)

Enterprise

For organisation-wide protection

Apply policy-based encryption and recipient authentication across your entire mail flow with our secure gateway.

Automated

For secure high-volume delivery

Send thousands of secure, authenticated emails automatically using rule-based triggers and system integrations.

Questions?

Talk to us

Book a demo with our team to see Mailock in action and get your questions answered.

Overcoming Barriers In Your Postal To Digital Communications Journey

Learn how to transition your financial services organisation from postal to digital communications, overcoming challenges, and reaping benefits.

Forging A Pathway to Carbon Zero with Cat Dillon

We explore how businesses can take big and small steps that align with their bottom line goals as well as helping to build a sustainable future.

Reassessing The ESG Hierarchy With Simon Pringle (Podcast)

We chatted with Professor Simon Pringle about the future of ESG (environmental, social, and governance) for podcast episode 7.